India Market Update April 1, 2026: Sensex Surges 1,187 pts (1.65%), Nifty +1.56% as Oil Prices Ease on Iran De-escalation Hopes | Gold, Silver, Mutual Funds, War News & BlissMoney Insights

Executive Summary

Indian benchmarks Sensex and Nifty opened FY27 on a strong note, surging over 1.5% in a sharp relief rally. This followed global markets' positive reaction to hopes of de-escalation in the ongoing West Asia (Iran) conflict. A drop in crude oil prices further boosted sentiment. Markets recovered from recent sharp losses amid geopolitical tensions, high oil prices, and FII outflows. Domestic institutions provided strong support. Bullion remained elevated on safe-haven demand but showed mixed moves on de-escalation signals. Mutual fund industry AUM stays at record levels with steady SIP flows. RBI's deferral of capital market exposure norms offered liquidity relief.

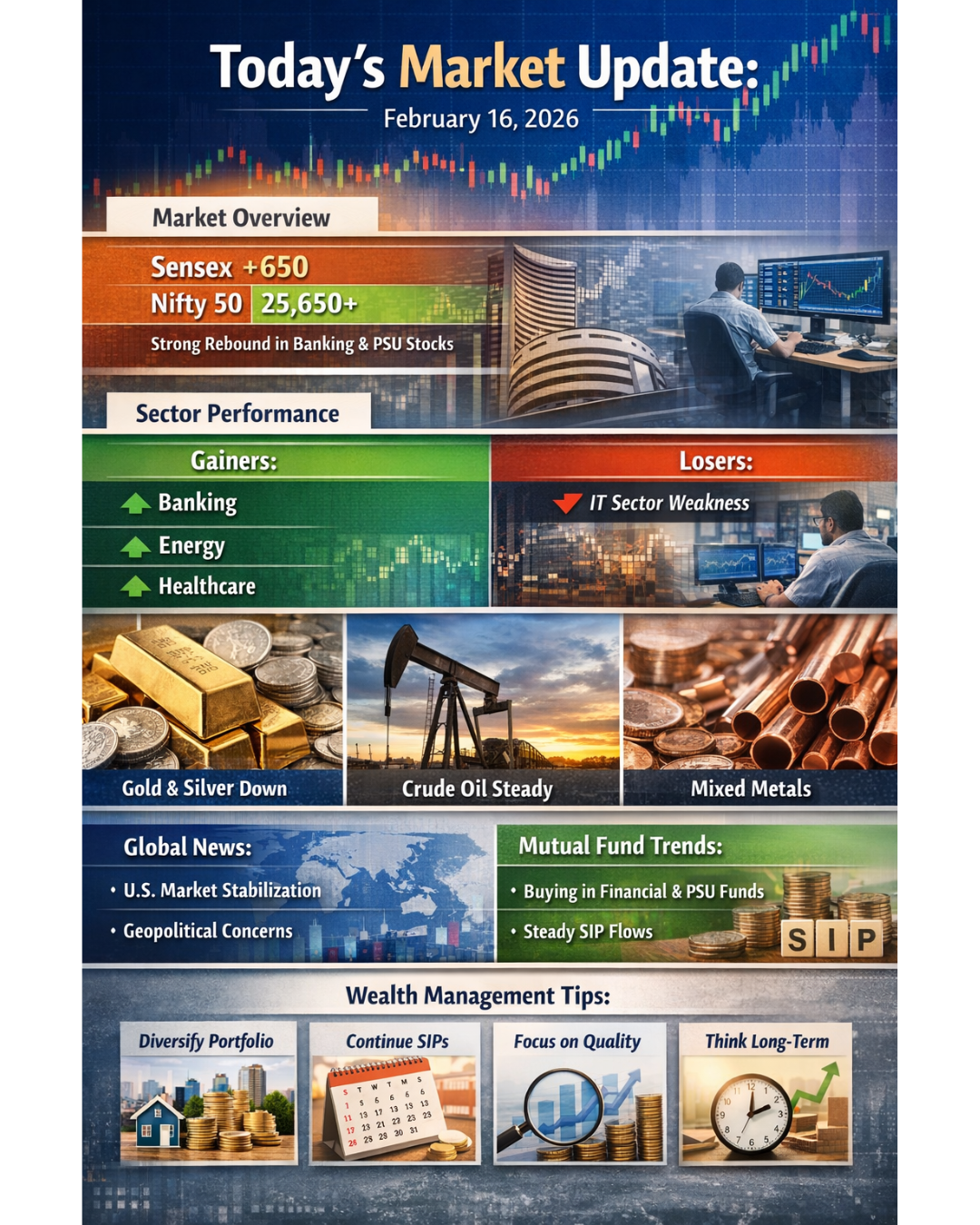

1. Key Indices (Closing, April 1, 2026)

- BSE Sensex: 73,134.32 ↑ 1,186.77 pts (+1.65%)

- NSE Nifty 50: 22,679.40 ↑ 348 pts (+1.56%)

- Sectoral Performance (outperformers): Banking, Media, Chemicals, Metals.

- Top Gainers (BSE): Trent, InterGlobe Aviation (IndiGo), Adani Ports, Bharat Electronics, SBI, Eternal.

- Top Losers (BSE): NTPC, Sun Pharma, Power Grid, UltraTech Cement, Bharti Airtel.

Institutional Flows (previous session reference):

- FIIs: Net sellers → ₹11,163 crore

- DIIs: Net buyers → ₹14,894 crore

Global cues were strongly supportive: Asian markets surged (Kospi +8.44%, Nikkei +5.24%), European indices positive.

2. Commodity Prices (April 1, 2026)

- Brent Crude: ~$103–103.7 per barrel (down ~0.22% intraday; eased on de-escalation hopes after recent spikes due to Iran conflict disruptions in Strait of Hormuz).

- WTI: Trading in the $97–98 range (futures data; exact spot aligned with Brent decline). Oil's drop supported Indian markets and rupee sentiment.

Gold & Silver (MCX & International)

- MCX Gold (per 10g): ₹1,52,007–1,52,137 ↑ 0.83–0.91%

- MCX Silver (per kg): ₹2,39,347–2,40,000 ↓ 0.26–0.75% (brief intraday surge to ₹2,42,250)

- International Spot Gold: ~$4,674–4,676/oz ↑ ~0.6%

- International Spot Silver: ~$74.79/oz ↓ ~0.17–0.89%

- Bullion rose ~3% this week on safe-haven buying amid the Iran conflict, though de-escalation signals (Trump's comments) led to some profit-taking in silver.

3. Market Updates & Sentiment

- Positive Drivers: Hopes of Iran war de-escalation (Trump indicated US operations could wind down in 2–3 weeks; conditional talks possible). Lower crude prices. Strong global risk-on mood.

- Broader Context: Markets rebounded from steep prior-session losses tied to geopolitical risks, FII outflows, and elevated oil. Banking/financials led gains amid RBI's supportive move on capital norms.

- Sentiment turned cautiously optimistic for FY27 start, though volatility remains due to ongoing global uncertainties.

4. Mutual Fund Update

- Industry AUM: Hit record ~₹82 lakh crore (Feb 2026 data; latest available). Equity AUM up ~29% YoY; hybrid and passive segments also strong.

- SIP Flows: Gross inflows ~₹29,845 crore/month (Feb; +15% YoY). Total SIP AUM ~₹16.64 lakh crore. Investor accounts continue rising (unique folios ~6.09 crore).

- Trend: Steady equity inflows (flexi-cap leading). Industry resilience evident despite market volatility; direct plans now ~49% of AUM. No major April 1-specific disruption reported.

5. Important Indian News Affecting Markets

- RBI Deferral of Capital Market Exposure Norms: Implementation postponed from April 1 to July 1, 2026. Provides relief to banks, brokers, and capital market intermediaries. Eases some lending/collateral rules temporarily (e.g., bank guarantees for brokers). Clarifications issued on acquisition finance and exposures. Positive for market liquidity and broker funding amid volatility.

- Other April 1 changes (minor impact): Updated PAN rules, SBI credit card cashback tweaks, FASTag/ATM norms, RuPay lounge access revisions.

- Rupee under pressure from oil and outflows; RBI monitoring corporate forex positions.

6. War/Geopolitical News (Impact on Markets)

West Asia/Iran Conflict (Primary Focus): Ongoing US-Israel vs Iran operations. Key developments today:

- Hopes of de-escalation rose after US President Trump stated the US “will be done attacking Iran probably in two to three weeks” and indicated openness to conditional wind-down.

- Strait of Hormuz disruptions affecting oil/shipping; some energy infrastructure hits reported.

- Markets cheered the signals → lower oil, higher equities globally.

- Russia-Ukraine: Ongoing but lower immediate market impact; remains a background risk for energy and inflation. Overall: Geopolitics drove recent volatility (oil spikes, FII selling), but today's de-escalation optimism triggered a broad relief rally.

7. Insights from BlissMoney (Bangalore-based Wealth Management Advisor)

- BlissMoney (expert in mutual funds, tax planning, and retirement) has consistently highlighted India’s structural growth story remaining intact despite global headwinds.

- Recent newsletters (March 23–28, 2026) noted: Markets under pressure from Gulf/Iran conflict, oil shock, and rupee volatility — yet India’s fundamentals (earnings resilience, domestic demand) provide a strong anchor.

- They flagged relief rallies as tensions ease and emphasized staying invested via SIPs in quality equity/hybrid funds.

- Perspective aligns with today’s move: Geopolitical noise creates volatility, but long-term India opportunity persists. Their advice focuses on diversified portfolios and rupee-cost averaging amid uncertainty.